Content

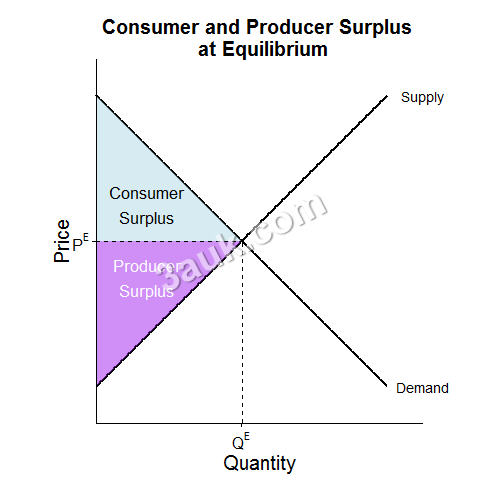

meaning and significance of consumer surplus

- Consumer surplus refers to the difference between the amount a consumer is willing to pay for a good or service and the actual price they pay for it.

- It is a measure of the welfare or benefit that a consumer derives from a transaction.

meaning and significance of producer surplus

- Producer surplus refers to the difference between the amount a producer is willing to accept for a good or service and the actual price received for it.

- It is a measure of the profit or benefit that a producer derives from a transaction.

causes of changes in consumer and producer surplus

- Changes in supply and demand: A shift in the demand curve or supply curve can cause changes in the market price and, in turn, changes in consumer and producer surplus. An increase in demand, for example, can raise the market price and increase producer surplus, while decreasing consumer surplus.

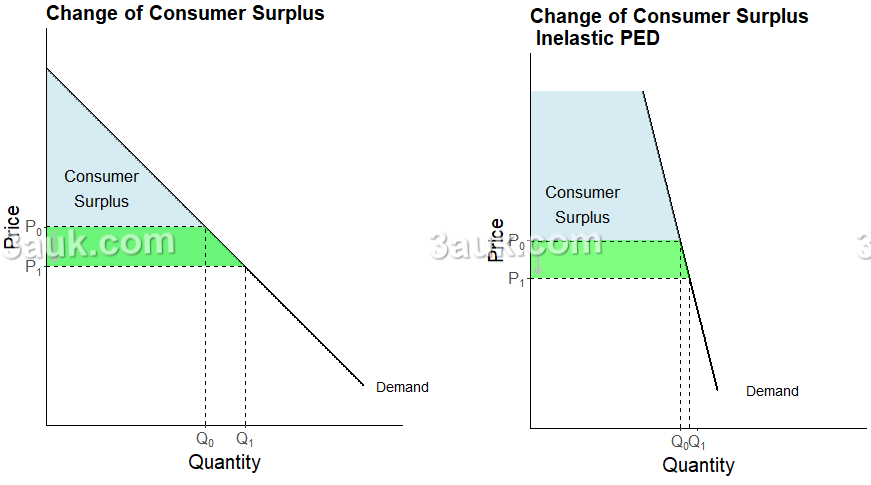

- Changes in price elasticity of demand and supply: The responsiveness of consumers and producers to changes in price can also impact consumer and producer surplus. If demand is more elastic, consumers are more sensitive to price changes and will purchase less at a higher price, leading to a decrease in consumer surplus.

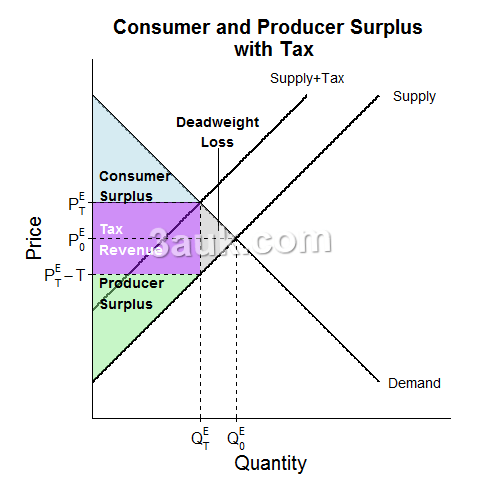

- Government policies: Government policies, such as taxes, subsidies, price controls, and tariffs, can impact consumer and producer surplus. For example, a tax on a good can increase its price, leading to a decrease in consumer surplus and an increase in producer surplus.

- Technological advancements: New technology can increase the supply of a good, lowering its price and increasing consumer surplus, while decreasing producer surplus.

- Changes in market structure: Changes in the number of firms in a market or the level of market competition can impact the market price and, in turn, consumer and producer surplus.

significance of price elasticity of demand and of supply in determining the extent of these changes

- If demand for a good is price elastic, a small change in price will result in a relatively large change in the quantity demanded, meaning consumers are sensitive to price changes.

- This can lead to a large decrease in consumer surplus with only a small increase in price.

- If demand for a good is price inelastic, a change in price will result in only a small change in the quantity demanded, meaning consumers are not very sensitive to price changes.

- In this case, consumer surplus may not change significantly even with a large change in price.

- If the supply of a good is price elastic, a small change in price will result in a relatively large change in the quantity supplied, which can lead to a large change in producer surplus.

- If the supply of a good is price inelastic, a change in price will result in only a small change in the quantity supplied, meaning producer surplus may not change significantly even with a large change in price.

Join the conversation