- Topic Questions (MCQ – EASY): Economic growth and sustainability

- Topic Questions (MCQ – HARD): Economic growth and sustainability

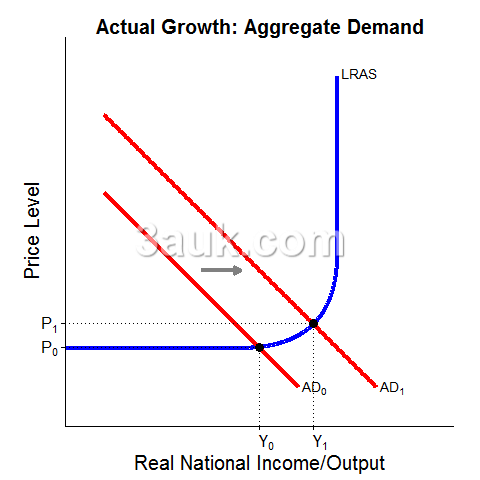

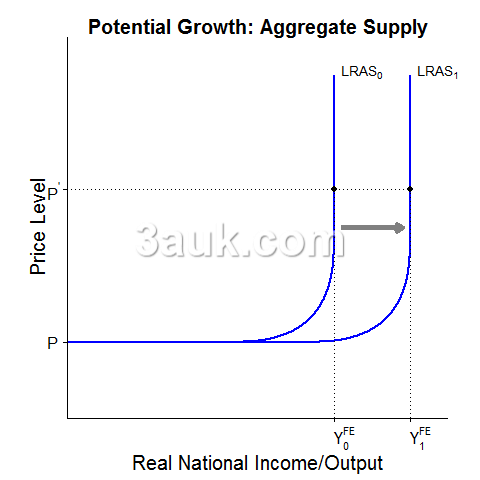

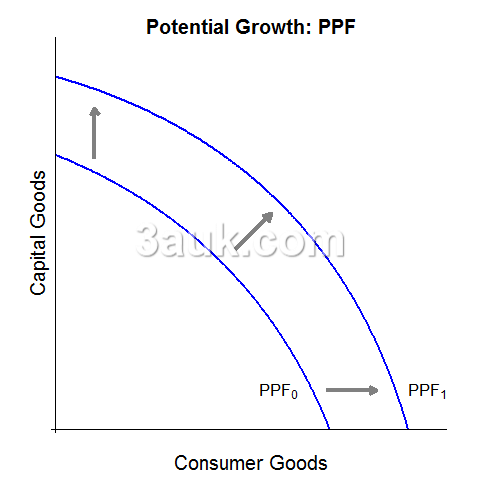

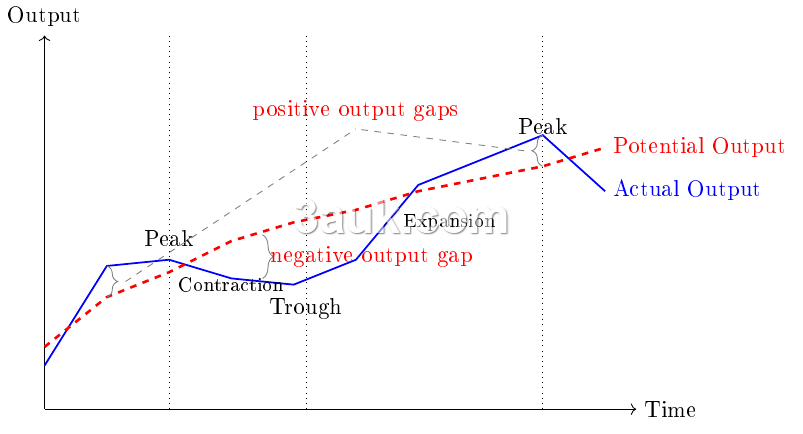

actual growth versus potential growth in national output

- Actual growth represents the observed or realized increase in the production of goods and services in an economy.

- It is often measured by the percentage change in real GDP from one period to another.

- Actual growth can be influenced by various factors such as changes in consumer spending, investment, government expenditure, and net exports.

- It reflects the current level of economic activity and output in an economy.

- Potential growth refers to the maximum sustainable rate at which an economy can grow over the long term without causing excessive inflation or imbalances.

- It represents the growth rate an economy can achieve when all resources are fully utilized, including labor, capital, and technology, without generating inflationary pressures.

- Potential growth is influenced by factors such as population growth, labor force participation, productivity, technological advancements, and investment in physical and human capital.

The difference between actual growth and potential growth is important because it provides insights into the economy's performance and its capacity for sustained expansion.

- If actual growth exceeds potential growth, it may lead to inflationary pressures and overheating of the economy.

- Conversely, if actual growth falls below potential growth, it may indicate underutilization of resources and a potential for economic improvement.

Policymakers and economists closely monitor the gap between actual and potential growth to assess the overall health of an economy and determine appropriate policy interventions.

- Sustainable economic growth aims to align actual growth with potential growth, ensuring a balance between expanding output and maintaining stability in prices and the overall economy.

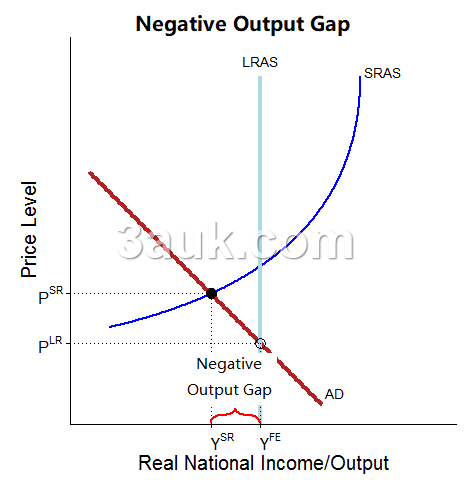

positive and negative output gaps

Positive and negative output gaps are concepts used in macroeconomics to analyze the difference between actual output (real GDP) and potential output in an economy.

- A positive output gap occurs when actual output exceeds potential output.

- It indicates that the economy is operating above its long-term sustainable level and is experiencing an expansionary phase.

- A positive output gap implies that there is upward pressure on prices and resources are being utilized at a higher rate, potentially leading to inflationary pressures.

- In this situation, the economy may be operating at or near full employment, and there may be shortages of labor and other resources.

- Policymakers often aim to close a positive output gap to maintain price stability and sustainable economic growth.

- A negative output gap occurs when actual output falls below potential output.

-

- It indicates that the economy is operating below its long-term sustainable level and is experiencing a contractionary phase.

- A negative output gap suggests that there is slack in the economy, with idle resources and high unemployment.

- It may also indicate that there is downward pressure on prices, leading to deflationary tendencies.

- Closing a negative output gap is a goal for policymakers as it represents a recovery towards full employment and maximum sustainable economic output.

Monitoring and analyzing output gaps help policymakers assess the overall health of the economy and make informed decisions regarding fiscal and monetary policies.

- Closing positive output gaps generally involves implementing contractionary measures to control inflation, while closing negative output gaps requires expansionary policies to stimulate economic activity and reduce unemployment.

- Achieving a balance between actual output and potential output is crucial for maintaining stable economic growth and avoiding imbalances in the economy.

business (trade) cycle: phases of the cycle; causes of the cycle; role of automatic stabilisers

The business cycle, also known as the trade cycle, refers to the recurrent pattern of expansion and contraction in economic activity over time.

- It is characterized by fluctuations in output, employment, and other key economic indicators.

- The business cycle is typically divided into four phases: expansion, peak, contraction, and trough.

-

- Expansion: During this phase, economic activity is growing, and key indicators such as GDP, employment, and consumer spending are increasing.

- Businesses are experiencing higher sales, and there is a general sense of optimism in the economy. Expansion is often accompanied by rising inflation as demand increases.

- Peak: The peak represents the highest point of economic activity in the business cycle.

- It marks the end of the expansion phase and usually coincides with the highest levels of employment, output, and consumer confidence.

- Prices may also reach their peak during this phase.

- Contraction: In the contraction phase, economic activity slows down, and key indicators begin to decline.

- Businesses may experience a decrease in sales, leading to reduced production and layoffs.

- Consumer spending and investment decline, and there is a general sense of pessimism in the economy.

- Contraction is often associated with falling prices or even deflation.

- Trough: The trough is the lowest point of the business cycle, representing the end of the contraction phase.

- Economic activity is at its lowest, with high unemployment rates and low output.

- However, the trough also signifies the beginning of a new cycle, as it sets the stage for recovery and expansion.

- Expansion: During this phase, economic activity is growing, and key indicators such as GDP, employment, and consumer spending are increasing.

The business cycle is influenced by various factors, including:

- Macroeconomic shocks: External events such as changes in global economic conditions, natural disasters, political instability, or financial crises can disrupt the normal functioning of the economy and lead to fluctuations in the business cycle.

- Monetary and fiscal policy: Government actions, particularly monetary policy implemented by central banks and fiscal policy enacted by governments, can have an impact on the business cycle. Interest rate changes, government spending, taxation, and regulatory policies can either stimulate or dampen economic activity.

- Investment and consumer confidence: Business and consumer sentiment play a significant role in shaping the business cycle. High levels of investment and consumer confidence can fuel expansion, while low confidence can lead to a contraction.

Automatic stabilizers are economic mechanisms that work to offset fluctuations in the business cycle.

- They function without explicit government intervention and help to stabilize the economy by dampening the effects of economic fluctuations.

- Examples of automatic stabilizers include progressive income taxes, unemployment benefits, and welfare programs.

- During economic downturns, automatic stabilizers increase government spending and provide income support to individuals and households, thereby boosting demand and mitigating the severity of recessions.

- In periods of expansion, automatic stabilizers work in the opposite direction, reducing government spending and limiting inflationary pressures.

policies to promote economic growth and their effectiveness

Policies to promote economic growth are designed to stimulate investment, increase productivity, and create favorable conditions for businesses to thrive. Here are some common policy measures and an assessment of their effectiveness:

- Monetary Policy: Central banks use monetary policy tools, such as interest rate adjustments and open market operations, to influence borrowing costs, inflation rates, and overall economic activity.

- By lowering interest rates, central banks aim to encourage borrowing and investment, which can stimulate economic growth.

- The effectiveness of monetary policy depends on various factors, including the prevailing economic conditions and the responsiveness of businesses and consumers to changes in interest rates.

- Fiscal Policy: Governments can implement fiscal policy measures, such as changes in taxation and government spending, to boost economic growth.

- Expansionary fiscal policies involve increasing government spending and/or reducing taxes to stimulate aggregate demand and encourage investment.

- However, the effectiveness of fiscal policy depends on factors like the size of the fiscal stimulus, the efficiency of government spending, and the impact on public debt levels.

- Infrastructure Investment: Investing in infrastructure projects, such as transportation networks, energy systems, and communication networks, can enhance productivity, attract private investment, and stimulate economic growth.

- Well-designed infrastructure investments can improve business efficiency, reduce transportation costs, and facilitate trade.

- However, the effectiveness of infrastructure investment depends on factors like the quality of project selection, funding mechanisms, and efficient project implementation.

- Education and Human Capital Development: Policies that prioritize education and skills development can have long-term positive effects on economic growth.

- Investing in education, vocational training, and research and development helps build a skilled workforce, fosters innovation, and improves productivity.

- However, the impact of these policies may take time to materialize, as it requires sustained investments and a focus on quality education and skills training.

- Trade Liberalization: Opening up markets through trade liberalization measures, such as reducing tariffs and trade barriers, can stimulate economic growth by promoting international trade, attracting foreign investment, and encouraging specialization.

- Increased trade can lead to productivity gains, access to new markets, and the transfer of technology and knowledge.

- However, the effectiveness of trade liberalization policies depends on the existence of a supportive domestic business environment and adequate infrastructure.

- Regulatory Reforms: Streamlining regulations, reducing bureaucratic hurdles, and improving the ease of doing business can enhance competitiveness and foster economic growth.

- Simplifying business registration processes, reducing administrative burdens, and ensuring transparent and predictable regulatory frameworks can attract investment, promote entrepreneurship, and facilitate business expansion.

- The effectiveness of regulatory reforms depends on the commitment of governments to implement and enforce them consistently.

It's important to note that the effectiveness of these policies can vary depending on the specific context, economic conditions, and the implementation strategies employed.

- A comprehensive and coordinated approach that combines various policy measures is often more effective in promoting sustained economic growth. Additionally, the success of these policies relies on sound governance, political stability, the rule of law, and a favorable business climate.

- Continuous evaluation and adjustment of policies based on evidence and feedback from stakeholders are crucial to maximizing their impact on economic growth.

inclusive economic growth

Inclusive economic growth refers to a form of economic development that benefits all segments of society, ensuring that the benefits of growth are widely shared and reach marginalized and vulnerable populations.

- Inclusive economic growth is characterized by sustainable and broad-based development that leads to improved living standards, reduced poverty, and decreased inequality.

- It aims to provide equal access to economic opportunities, resources, and social services, regardless of individuals' socioeconomic backgrounds, gender, ethnicity, or geographical location.

- Inclusive growth focuses on reducing disparities, fostering social cohesion, and ensuring that marginalized groups have the chance to participate and benefit from the growth process.

Impact of Economic Growth on Equity and Equality:

- Economic growth can have both positive and negative impacts on equity and equality.

- On one hand, sustained and robust economic growth can create opportunities for income generation, job creation, and poverty reduction, leading to improved equity and equality.

- It can provide resources for public investment in education, healthcare, and social protection, contributing to a more equitable society.

- However, if the benefits of growth are concentrated in the hands of a few, it can exacerbate inequality and lead to social exclusion.

- Therefore, inclusive economic growth seeks to ensure that the benefits are distributed more equitably, addressing disparities and promoting social inclusion.

- On one hand, sustained and robust economic growth can create opportunities for income generation, job creation, and poverty reduction, leading to improved equity and equality.

Policies to Promote Inclusive Growth: Various policy measures can be implemented to promote inclusive economic growth.

- Targeted Social Programs: Implementing social protection programs, such as cash transfers, subsidies for basic needs, and access to quality healthcare and education, can help reduce poverty and inequality by providing support to vulnerable populations.

- Enhancing Education and Skills Development: Investing in education and skills development programs that are accessible, affordable, and of high quality can empower individuals and improve their employment prospects, leading to more inclusive economic growth.

- Promoting Financial Inclusion: Facilitating access to financial services, such as banking, credit, and insurance, for marginalized and underserved populations can enable them to participate in economic activities, save, invest, and manage risks.

- Labor Market Policies: Implementing policies that promote fair and inclusive labor markets, such as minimum wage regulations, anti-discrimination laws, and protection of workers' rights, can contribute to reducing income disparities and improving social mobility.

- Support for Small and Medium Enterprises (SMEs): Providing targeted support, such as access to finance, business development services, and technical assistance, to SMEs can foster entrepreneurship, job creation, and economic diversification, benefiting marginalized communities.

- Infrastructure Development: Investing in infrastructure projects, particularly in underserved regions, can enhance connectivity, improve access to markets and services, and create employment opportunities, promoting inclusive growth.

- Empowering Women and Addressing Gender Inequality: Implementing policies that promote gender equality, such as ensuring equal access to education, healthcare, and economic opportunities, can foster inclusive growth by unlocking the full potential of women as drivers of economic development.

- Stakeholder Engagement and Participatory Decision-Making: Promoting inclusive growth requires active engagement and participation of all stakeholders, including civil society organizations, marginalized communities, and vulnerable groups, in the decision-making processes and policy formulation.

Policy coherence, effective governance, and monitoring mechanisms are crucial to ensure that policies are effectively implemented and their impact on inclusivity is regularly assessed.

sustainable economic growth

Sustainable economic growth involves achieving continuous economic progress while ensuring the preservation of natural resources, protecting the environment, and promoting social equity.

- It focuses on meeting the needs of the present generation without compromising the ability of future generations to meet their own needs.

- It takes into account economic, social, and environmental considerations in decision-making processes.

Using and Conserving Resources

- Sustainable economic growth emphasizes the efficient and responsible use of resources.

- This includes minimizing waste generation, promoting recycling and reuse, adopting cleaner production methods, and embracing renewable energy sources.

- Conserving resources ensures their availability for future generations and reduces the environmental impact associated with resource extraction and consumption.

Impact of Economic Growth on the Environment and Climate Change

- Economic growth, particularly in resource-intensive industries, can have adverse environmental effects.

- Increased production and consumption can lead to higher levels of pollution, deforestation, habitat destruction, and greenhouse gas emissions, contributing to climate change and biodiversity loss.

- Unsustainable practices, such as overexploitation of natural resources and reliance on fossil fuels, can undermine the long-term health of ecosystems and compromise the well-being of both present and future generations.

Policies to Mitigate the Impact of Economic Growth on the Environment and Climate Change:

Governments and international organizations recognize the need to implement policies that promote sustainable economic growth.

- Environmental Regulations and Standards: Establishing and enforcing regulations to control pollution, protect natural resources, and mitigate climate change.

- This includes setting emissions limits, promoting renewable energy sources, and implementing sustainable land and water management practices.

- Incentives for Green Technologies and Practices: Providing financial incentives, such as tax breaks or subsidies, to encourage businesses and individuals to adopt environmentally friendly technologies, reduce emissions, and promote sustainable practices.

- Sustainable Urban Planning: Implementing urban planning policies that prioritize energy efficiency, public transportation, green spaces, and sustainable infrastructure.

- This can help reduce congestion, improve air quality, and enhance the quality of life in cities.

- Conservation and Biodiversity Protection: Implementing measures to preserve and restore ecosystems, protect endangered species, and promote sustainable forestry and fisheries practices.

- International Cooperation and Agreements: Collaborating with other nations to address global environmental challenges, such as climate change, through agreements like the Paris Agreement.

- This includes setting targets for emissions reduction, promoting renewable energy investments, and supporting climate adaptation efforts.

- Public Awareness and Education: Raising awareness about the importance of sustainable practices and providing education on environmental issues.

- This can foster a culture of sustainability and encourage individuals to make informed choices in their daily lives.

It's important to note that achieving sustainable economic growth requires a comprehensive and coordinated approach that balances economic development, social well-being, and environmental protection.

- It involves integrating sustainability considerations into policy-making, promoting green innovation and technology, and engaging all stakeholders, including businesses, civil society, and individuals, in the transition to a more sustainable and resilient future.