Content

short run and long run analysis: output, profits, entry and exit, efficiency

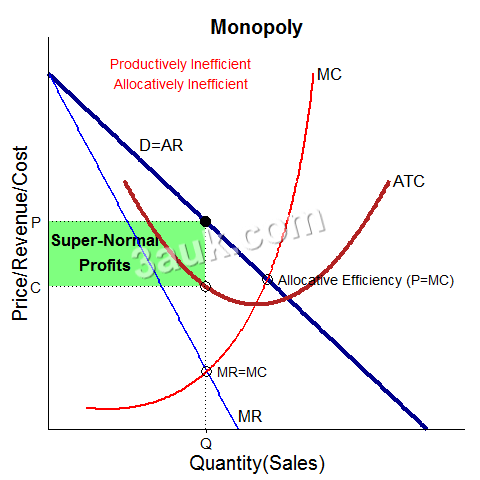

- In the short run, a monopolist can choose the level of output that maximizes profit, which occurs at the point where marginal revenue equals marginal cost. However, the price charged will be higher than the marginal cost, resulting in a deadweight loss to society.

- In the long run, a monopolist can earn positive economic profit due to the barriers to entry, which prevents new firms from entering the market and competing away the profits. The monopolist may also choose to invest in research and development, leading to innovation and improvement in products.

- However, the monopolist's behavior may not lead to allocative efficiency, as the price charged is higher than the marginal cost, resulting in a loss of consumer surplus. The lack of competition may also lead to a lack of productive efficiency (x-inefficiency), as there is no pressure to minimize costs.

how may monopolies arise

Monopolies can arise due to several factors such as:

- Control over essential resources: A firm that controls an essential resource required to produce a good or service may become a monopoly in that market. For example, a firm that controls a particular mine of a rare mineral required for a specific product can become a monopoly in that industry.

- Government-granted monopoly: Governments may grant exclusive rights to a company to produce and sell a particular good or service for various reasons such as national security or public interest. These are known as legal monopolies.

- Economies of scale: A firm may become a monopoly if it can achieve economies of scale, meaning it can produce goods or services at a lower cost than its competitors due to the high volume of production. This may make it difficult for new firms to enter the market and compete.

- Intellectual property: A firm that holds a patent for a particular product or process may become a monopoly in that industry until the patent expires.

- Predatory pricing: A firm may use predatory pricing strategies, such as setting prices below the cost of production, to drive its competitors out of business and gain a monopoly in the market.

Natural monopoly

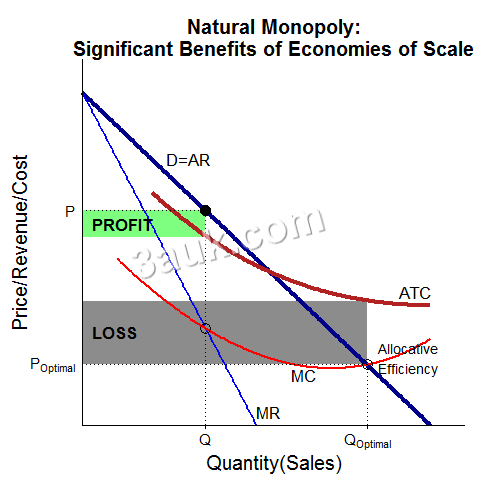

A natural monopoly exists when it is most efficient for production to be carried out by a single firm, due to high fixed costs of production.

- This can occur in industries where there are significant economies of scale, such as in the provision of utility services like water, gas, and electricity.

- In a natural monopoly, the costs of production decrease as the quantity of output increases, and the firm's average total cost (ATC) curve continually decreases, which creates a barrier to entry for other firms.

- The result is that the existing firm can produce the entire output for the market at a lower cost than any potential new entrant, and so competition is restricted.

- A natural monopoly will produce at the point where marginal cost (MC) intersects marginal revenue (MR), which is also where MC intersects the firm's average total cost (ATC) curve.

- This will result in a higher price than the competitive price, but a lower quantity of output. This will lead to a deadweight loss, as consumer surplus is reduced, and there is a loss of allocative efficiency.

- To address the inefficiencies of a natural monopoly, regulation may be imposed by the government, with the aim of promoting competition and efficiency. This can take the form of price regulation or the imposition of average cost pricing, where the price charged by the natural monopoly is equal to its average total cost, plus a fair rate of return.

Join the conversation