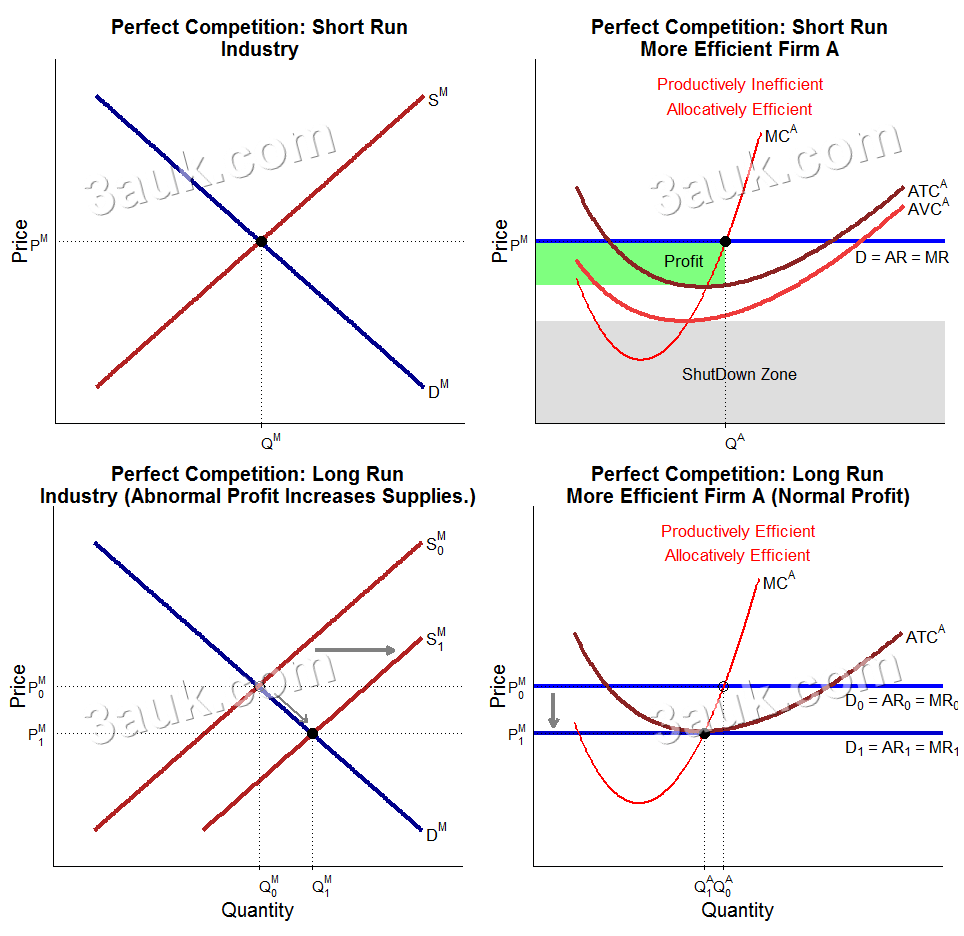

Long-run equilibrium in a perfectly competitive market occurs when all production factors can change, and firms earn only normal profit. At this stage, there is no incentive for new firms to enter or existing firms to leave the market.

Key conditions at long-run equilibrium:

- P = MR = MC: This ensures profit maximization.

- P = minimum ATC: This ensures that firms earn zero economic profit (no supernormal profit).

- P = minimum AC: This ensures productive efficiency.

How the market reaches this state:

- If firms earn short-run supernormal profits, new firms enter the market. This increases total supply and lowers the market price.

- If firms face short-run losses, some firms exit the market. This decreases total supply and raises the market price.

- This process repeats until the price equals the minimum average cost, resulting in zero economic profit.

Efficiency at long-run equilibrium:

- Allocatively efficient: Price equals marginal cost (P = MC), meaning resources are used to produce what consumers want.

- Productively efficient: Goods are produced at the lowest possible cost.

- No X-inefficiency: There is no waste in the production process.

This state is considered the ideal outcome for a perfectly competitive market.

Categories: