Perfect competition is a market structure where many buyers and sellers trade identical products. In this market, no single firm has the power to control or influence prices, and all participants have access to complete information.

Key features include:

- Many buyers and sellers: No individual firm is large enough to influence the market price.

- Homogeneous products: Goods are identical, meaning customers see no difference between items from different sellers.

- Free entry and exit: There are no barriers for new companies to start selling or for existing companies to leave the market.

- Perfect information: Everyone knows all the details about product quality and market prices.

- Price takers: Every firm accepts the market price set by supply and demand.

- Profit maximization: Firms aim to make the most profit where Marginal Revenue (MR) equals Marginal Cost (MC).

Conditions for long-run equilibrium:

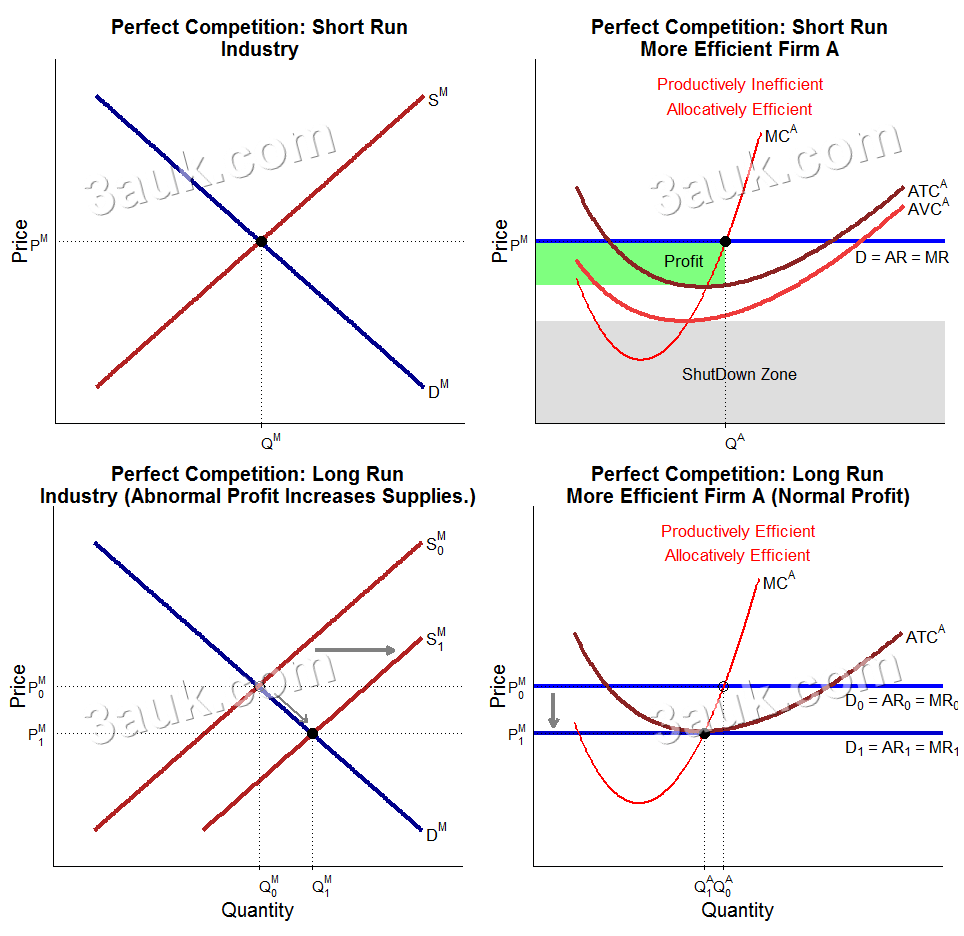

In the long run, firms in perfect competition only earn normal profit. If companies make extra (supernormal) profits, new firms enter the market, which increases supply and lowers the price. If companies make losses, some will leave the market, which decreases supply and raises the price. This results in an equilibrium where Price = Marginal Cost = Average Cost.

- Allocatively efficient: Resources are used to produce what people want (Price = Marginal Cost).

- Productively efficient: Goods are produced at the lowest possible cost.

Categories: